Source: RyanKing999/iStock via Getty images.

Multiprocessor payment architectures, where merchants intentionally distribute transaction volume across multiple processors or acquiring banks rather than relying on a single provider, are no longer an edge-case strategy. The percentage of merchants that prefer a multiprocessor setup has grown from 50% in 2023 to 62% in 2025, according to a study conducted by 451 Research by S&P Global.

What was once a reactive response to geographic expansion or processor limitations has evolved into a deliberate portfolio approach to payments — one that prioritizes performance optimization, scalability, redundancy and flexibility. In parallel, more than 60 vendors now offer payment orchestration platforms designed to abstract operational complexity and maximize the outcomes of a multiprocessor strategy.

The Take

Multiprocessor architectures are becoming the default design model for scaled digital commerce. As merchants diversify processors to optimize performance, manage risk and retain control over their payments strategy, orchestration shifts from optional tooling to tactical infrastructure. However, its value is not universal. Payment orchestration delivers the strongest return when transaction scale, geographic expansion and operational complexity converge. At that point, orchestration shifts from an optional abstraction layer to a strategic necessity.

Payment orchestration market opportunity

451 Research’s Payment Orchestration Market Monitor & Forecast reflects the growing trend of merchants aiming to optimize their multiprocessor environments.

We estimate the global market for payment orchestration platforms reached approximately $2.13 billion in revenue by the end of 2025 and is projected to grow to $4.72 billion by 2029, representing a compound annual growth rate of 25.5%.

However, demand for third-party payment orchestration is not universal. While multiprocessor preference is rising, the economic and operational value of orchestration crystallizes only at specific scale and complexity thresholds. For some merchants, it is strategic infrastructure; for others, it remains unnecessary overhead.

The scale inflection point

Payment volume is a critical variable in assessing payment orchestration readiness. At lower volumes, simplicity tends to dominate payments strategy. Merchants under $100 million in annual online sales often operate with a limited geographic footprint and are served reasonably well by a single processor. For this cohort, integration ease and bundled functionality generally outweigh the marginal gains from sophisticated routing optimization or extensive processor diversification.

As merchants approach $100 million-$500 million in annual online volume, geographic expansion and authorization performance begin to matter more materially. Some begin experimenting with multiple processors or adding local payment methods. However, orchestration adoption remains selective and often tied to a specific expansion initiative rather than a structural redesign of the payments stack.

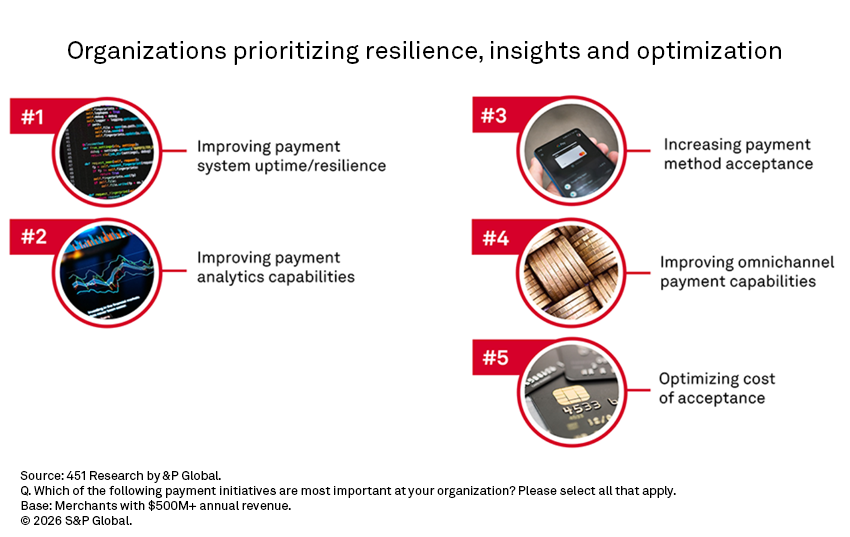

We find that the most pronounced adoption occurs between $500 million and $2 billion in online volume. At this stage, merchants are large enough to justify multiprocessor strategies and more sophisticated cross-border infrastructure, yet typically lack the internal payments engineering depth to build and maintain a proprietary orchestration layer. The cost of managing disparate integrations, reconciliation systems, and routing logic often begins to exceed the cost of outsourcing orchestration to a specialized provider. A recent study conducted by 451 Research shows that priorities of merchants with upward of $500 million in annual revenue — including improving payment system uptime/resilience, improving payment analytics capabilities, and increasing payment method acceptance — map well to the outcomes associated with payment orchestration.

Organizational merchants processing $2 billion-$10 billion annually often face a different dynamic: They may already operate homegrown routing systems built years prior. For this segment, adopting a third-party payment orchestration platform is frequently framed as modernization — replacing brittle internal logic, consolidating global reporting, and enabling faster integration of new providers.

Above $10 billion in volume, some mega-organizations maintain highly effective internal orchestration capabilities, though even this group increasingly evaluates third-party platforms for agility, resilience and cost efficiency.

Merchant profiles best-suited for orchestration

Although no single industry dominates payment orchestration, adoption consistently correlates with structural complexity. Complexity may stem from geography, business model, regulatory exposure, monetization structure or organizational design. Where that complexity intersects with meaningful payment volume, orchestration becomes strategically relevant.

Global and cross-border merchants. Global retailers, travel providers and hospitality groups operate across currencies, regulatory regimes and domestic acquiring markets. As they expand, they inevitably accumulate multiple processors and local payment methods, which creates integration sprawl and reporting fragmentation. Payment orchestration enables intelligent domestic routing, cross-border optimization and centralized data visibility across markets. For these merchants, orchestration becomes a margin-expansion and expansion-enablement tool rather than a back-office enhancement.

Subscription and recurring revenue businesses. Software-as-a-service (SaaS) platforms, streaming services and membership models depend on recurring payments and predictable renewal cycles. Their primary payments challenge is involuntary churn caused by card expiry, insufficient funds and issuer-driven declines. Orchestration supports intelligent retry sequencing, token portability and credential lifecycle management across multiple processors. This materially improves renewal recovery rates and preserves customer lifetime value. In this segment, orchestration functions as a revenue defense mechanism tied directly to retention economics.

High-risk or regulated industries. Gaming, crypto, digital assets and certain fintech models face volatile processor appetite and regulatory scrutiny. These businesses are particularly exposed to processor concentration risk and potential deplatforming. Payment orchestration enables diversified processing relationships and rapid traffic redistribution when provider constraints emerge. It also supports segmentation strategies that isolate risk across geographies or product lines. For these merchants, orchestration serves as continuity infrastructure that stabilizes revenue streams in uncertain environments.

Marketplaces and platform ecosystems. Marketplaces and gig platforms manage multiparty payment flows between buyers, sellers and service providers across regions. Their complexity extends beyond acceptance to include settlement, sub-merchant onboarding and cross-border payout considerations. Orchestration centralizes routing and reporting while preserving flexibility at the endpoint level. As platforms scale, this abstraction layer prevents integration debt from compounding. In this context, orchestration underpins operational scalability and ecosystem growth.

Multi-brand and acquisition-driven organizations. Organizations that grow through acquisition often inherit fragmented payment stacks across brands and regions. Over time, this creates inconsistent authorization performance, limited cross-brand benchmarking and duplicated integrations. Payment orchestration provides a harmonization layer that standardizes governance and reporting without requiring immediate provider consolidation. It allows corporate leadership to maintain centralized oversight while enabling regional flexibility. For these organizations, orchestration is frequently a post-merger integration accelerator.

Omnichannel retailers. Retailers operating across digital and physical channels increasingly require unified payment data and token portability across environments. Without orchestration, online and in-store systems often remain siloed, limiting customer identity continuity and performance optimization. Orchestration enables centralized routing logic and normalized reporting across card-present and card-not-present flows. This unified visibility supports more sophisticated analytics and customer lifecycle strategies. As omnichannel convergence deepens, orchestration becomes connective infrastructure rather than optional optimization.

Rapidly scaling growth-stage organizations. Companies transitioning from mid-market to upper mid-market volume frequently outgrow single-processor architectures faster than anticipated. Expansion into new geographies, the addition of alternative payment methods and authorization plateaus create structural strain on legacy integrations. Payment orchestration abstracts these integrations and reduces developer time spent maintaining payments infrastructure. This allows engineering teams to refocus on core product innovation while preserving flexibility. For high-growth organizations, orchestration is often a scalability enabler that prevents payments from becoming a growth bottleneck.

The Smart Home Era is Here

Want insights on consumer technology trends delivered to your inbox? Join the 451 Alliance.