Source: A. Martin UW Photography/Moment via Getty images.

Stablecoins have found early product-market fit in crypto-native and infrastructure-level use cases, but consumer payments remain the most uncertain — and most contested — frontier. Despite the promise of faster, cheaper and always-on money movement, limited consumer awareness and confidence raise open questions about whether stablecoins can meaningfully alter everyday payment behavior.

To assess the size and shape of the consumer opportunity, 451 Research by S&P Global surveyed US respondents on stablecoin awareness, appeal, use-case interest and adoption barriers. This research comes as stablecoins begin moving beyond crypto-native environments, with payment providers, card networks, and large banks actively testing stablecoin-based settlement, wallets and payment flows. The findings point to a market that is early, uneven and highly segmented.

The Take

Stablecoins are not yet poised for universal consumer adoption, but they show potential to carve out relevance with younger generations that already live in app-centric financial ecosystems. The opportunity for providers lies less in evangelizing the concept and more in using them invisibly to solve concrete problems: faster payments, cheaper transfers and seamless digital financial experiences. Those that can tightly embed stablecoins into familiar financial moments rather than requiring consumers to learn or adopt something entirely new will likely define the early phase of consumer adoption.

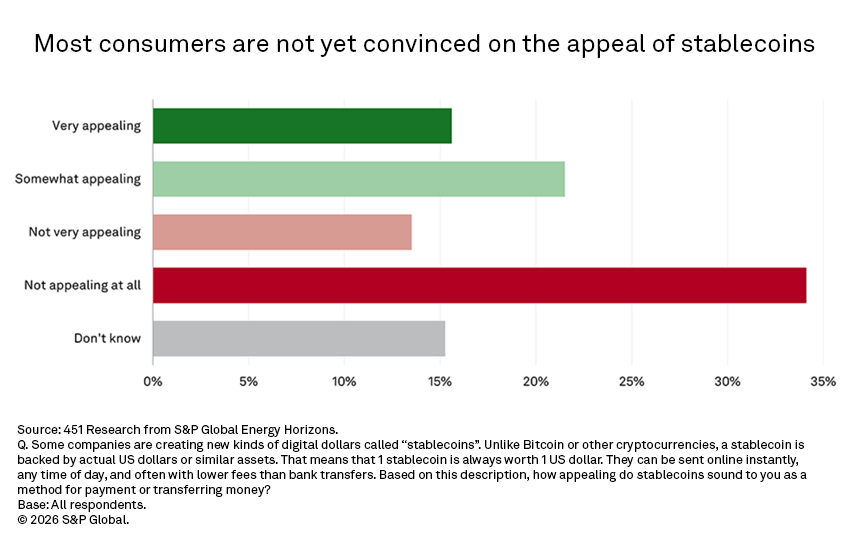

Overall appeal: Curiosity meets caution

Today, most consumer exposure to stablecoins remains concentrated within crypto exchanges rather than mainstream banking or payment apps. With only 11% of consumers having engaged in any cryptocurrency activity, such as buying, selling and trading, in the past 90 days, the addressable audience for organic stablecoin discovery remains small. This helps explain why awareness is still limited, despite growing investment and experimentation across the payments industry. Just 12% of consumers say they are familiar with stablecoins, rising to 20% among millennials.

Consumer appeal for stablecoins is sharply divided by age. Once provided a definition, 37% of consumers find the concept of stablecoins appealing (very or somewhat appealing), while nearly half (48%) say they are not appealing. This top-line figure, however, masks a pronounced generational divide.

- Generation Z and millennials stand out as the early audience. A majority of millennials (57%) and Gen Z (58%) find stablecoins appealing, with nearly a third of millennials (31%) describing them as very appealing — nearly twice the overall average.

- Generation X and older consumers tilt strongly negative. Among baby boomers and the Silent Generation, a majority at 60% and 65%, respectively, say stablecoins are “not appealing at all.”

This divide reflects a broader pattern seen across fintech adoption: Younger consumers are consistently more open to emerging financial services. As a point of reference, 20% of Gen Z report using buy-now, pay-later (BNPL) services in the past six months, compared with just 3% of baby boomers.

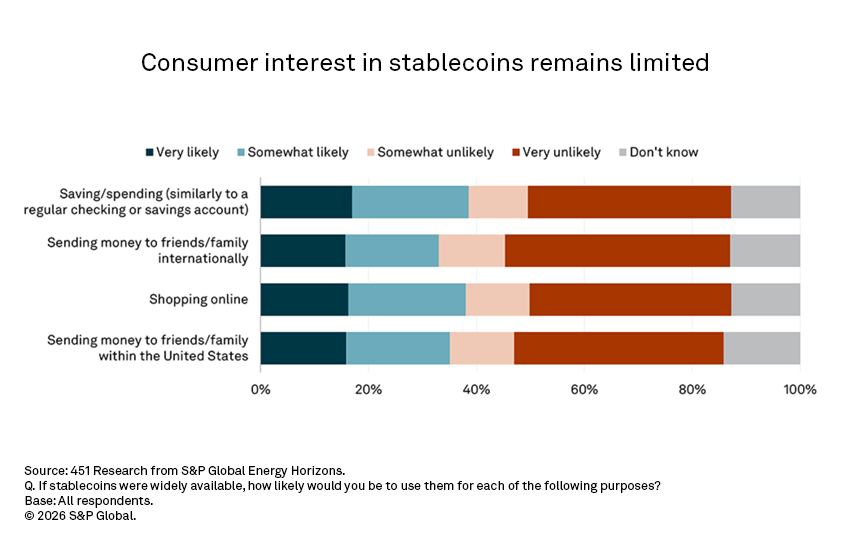

When assessing the early potential of specific stablecoin use cases, interest in using stablecoins for e-commerce follows a similar generational arc. More than a quarter of millennials (29%) and roughly a fifth of Gen Z (21%) indicate they would be very likely to use stablecoins for online shopping if they were widely available. Older consumers overwhelmingly reject the idea, with just 7% of baby boomers expressing the same intent.

For merchants, this suggests that stablecoin acceptance will initially matter most for brands serving younger, digitally native, and often cross-border customer bases rather than the mass market. Early merchant experimentation reflects this dynamic, with e-commerce platforms and payment processors selectively enabling stablecoin payments to test demand without materially reshaping core checkout experiences.

Cross-border payments are often cited as a core stablecoin use case — and the data supports this, particularly among younger cohorts. A quarter of Gen Z and 28% of millennials say they would be very likely to use stablecoins for international transfers, compared to just 3% of baby boomers. This underscores that stablecoins may gain traction fastest where traditional banking frictions are most visible to consumers, such as the time and cost associated with remittance.

Among all tested use cases, international transfers stand out as the clearest alignment between consumer interest and existing market momentum. Domestic peer-to-peer transfers show similar levels of interest, reinforcing that money transfers are a natural entry point for consumer adoption.

Using stablecoins as a substitute for a checking or savings account is the most ambitious — and most polarizing — use case. A quarter of Gen Z and 30% of millennials say they would be very likely to use stablecoins in this way. For Gen X and older generations, resistance is overwhelming, with roughly two-thirds of Boomers saying they would be very unlikely.

This use case is closely tied to the role of yield in evolving stablecoins from a payments instrument into a more bank-adjacent product that increasingly functions as transactional and yield-bearing store of value. The outcome of ongoing policy debates, particularly around stablecoin regulation and broader market structure frameworks such as CLARITY, will dictate how quickly stablecoins can function as true banking substitutes. Until those questions are resolved, stablecoins are more likely to complement traditional banking than replace it.

Barriers to adoption: Trust matters

Concerns about stablecoins are widespread across all age groups, even among those most interested.

The top concerns include:

- Fraud and scams (45%) — the leading worry overall, intensifying with age.

- Lack of necessity (43%) — many consumers, especially older ones, see no compelling reason to switch from existing money movement tools.

- Safety of funds (41%) — fears of loss, hacking, or technical failure remain salient.

Younger consumers are consistently less concerned across most dimensions, particularly around fraud, trust and regulation. However, even among millennials, fewer than one in six say they have no concerns at all. This highlights a critical reality: Interest does not equal confidence. Adoption will depend as much on education, branding and perceived safeguards as on technical performance. Notably, these concerns map closely to the protections consumers already associate with banks and major payment networks, reinforcing that adoption will hinge on who offers stablecoins as much as how they work.

Market implications

In the near term, the consumer stablecoin opportunity is less about scaling users and more about choosing the right entry points. With that in mind, three dynamics stand out:

Taken together, these dynamics suggest that consumer stablecoin adoption will be evolutionary rather than disruptive. Progress will be driven less by convincing consumers to care about stablecoins and more by making stablecoins quietly useful within financial experiences consumers already trust.

Takeaways for financial institutions and payment service providers

Consumer interest is concentrated among younger cohorts, signaling a future shift in expectations around speed, programmability, and the availability of money movement rather than near-term balance sheet disruption. Today, payments modernization is the primary defensive strategy for financial institutions. Improving real-time payments, cross-border transfers, and digital wallet experiences may matter more in the near term than launching consumer-facing stablecoins, particularly for retaining younger customers. Until clearer regulatory frameworks emerge, banks are likely to see greater value in stablecoins as infrastructure and settlement tools rather than retail banking replacements. For payment service providers (PSPs), the stablecoin opportunity is less about launching a new payment method and more about quietly modernizing how money moves. PSPs can create near-term value by applying stablecoins as infrastructure to improve international payouts, merchant settlement, and treasury operations — areas where merchants already feel pain. Those that emphasize fraud protection, compliance, and regulatory alignment will be best positioned to see stablecoin traction. While broad consumer pull is unlikely in the near term, PSPs should be positioned to scale consumer-facing use cases quickly if demand accelerates.

FinOps and the future of cloud spending automation

Want insights on fintech trends delivered to your inbox? Join the 451 Alliance.