Source: Group 10 0094_Large/S&P Global Media Portal via S&P Global.

Consumer interest in wearable technology held steady in 2025, with middle-income households carrying the torch. Both lower-income and higher-income households experienced slight year-over-year declines in planned buying, while middle-income, a rarely discussed group, saw an increase. Gen Z and millennials continue to be the dominant demographics driving wearable usage, with Gen Z particularly well-positioned as more of the cohort reaches adulthood.

The recent excitement over Apple’s entrance into the virtual reality space seems to have cooled, and is being somewhat replaced with a newfound interest in smart eyewear. The previous failures of Google Glass left the space ostensibly rudderless, but new AI-powered entrants, especially the Meta-Ray-Ban partnership, have created a resurgence among consumers.

This blog post presents the findings of a survey conducted by 451 Research from S&P Global Energy, which asked US consumers about their device ownership and buying plans.

Key takeaways from the survey

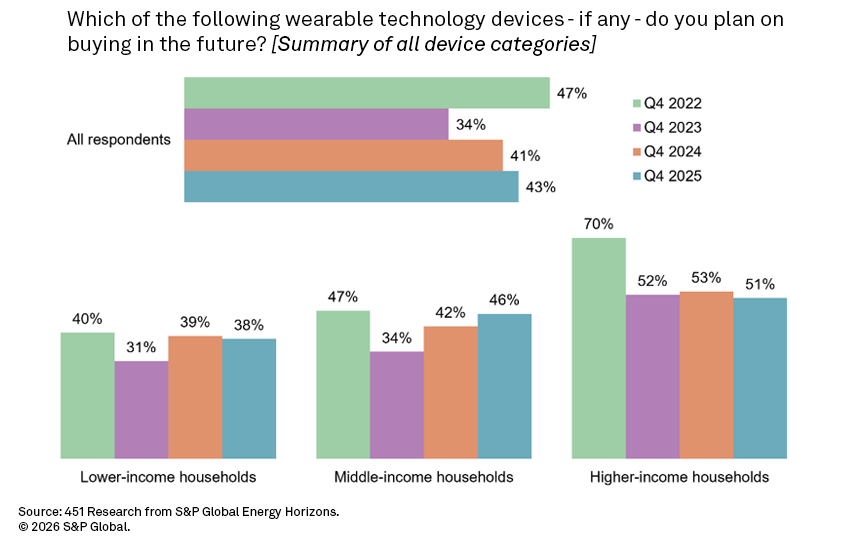

Wearable device buying holds steady. After a couple of years of seesawing demand, our Q4 2025 survey shows a more stable outlook for wearable-technology buying among consumers. According to the results, 43% of respondents plan to buy a wearable device in the future, which is a slight 2 points higher than Q4 2024. Overall, consumers cited electronics as a category they were likely to take advantage of during holiday sales, and wearables seem to be benefiting from this wave.

Middle-income households key to maintaining stable outlook. Planned spending among lower-income households (less than $50,000 per year; 38%; down 1 point) is on par with last year. The same can be said of higher-income households (more than $100,000 per year; 51%; down 2 points). So, how is there a slight increase in overall buying intent? As it turns out, middle-income households (between $50,000 and $100,000 per year; 46%) — a group rarely discussed in detail — are showing a 4-point increase in buying intent compared with the previous Q4 2024 survey. This improvement is enough to offset the slight declines seen in the other income groups.

Smartwatches, earbuds, headphones and fitness trackers remain most sought-after wearable devices. Looking at the specific wearable device types garnering the most consumer interest, the survey shows smartwatches (17%), smart earbuds (12%), smart headphones (11%) and fitness trackers (11%) as the devices respondents are most likely to buy in the future. Importantly, even with the increase in overall spending plans among middle-income households, there is still a clear imbalance in spending power. Of the 11 wearable tech categories we follow, higher-income households have double-digit purchasing plans in eight of these categories, compared with only four for middle-income households and two for lower-income ones.

Generation Z leads in wearable usage. Similar to planned buying, smartwatches, smart earbuds, fitness trackers and smart headphones are currently the most owned wearable devices among all respondents. Yet, preferences clearly differ by age. Throughout the last year, Gen Z has overtaken millennials as the top cohort using wearable devices. They are now the top users of nine device categories, with smartwatches (39%), smart earbuds (36%) and smart headphones (31%) leading the way. For their part, millennials are the top users of fitness trackers (19%) and are tied with Gen Z in personal safety devices (13%). They are also the second biggest users of every other device category.

Virtual- and augmented-reality demand levels off. The initial wave of new demand created by Apple’s entrance into the VR/AR headset space appears to have settled down. After an uptick in demand in the previous Q4 2024 survey, the current results show adoption of VR/AR headsets (7%) is unchanged year over year. The same is true of planned buying for these devices (7%; unchanged). The simple truth is that adoption is muted by device prices and the lack a gamechanger use case to drive uptake.

Meta’s Quest (38%) still captures the largest share of the VR/AR headset market, with Apple (19%) garnering a solid second-place share after only a short time on the market. Samsung (15%) and Sony (14%) are the only other manufacturers with double-digit ownership.

Is smart eyewear the next big thing? A couple of years ago, this was the question surrounding virtual reality. As that area has cooled off a bit, demand for smart eyewear is showing a resurgence. In fact, smart eyewear (8%) has leapt past VR/AR headsets (7%) among consumers planning to buy wearable devices in the future, albeit by a narrow margin. Smart eyewear is likely getting a boost due to more practical use cases in daily life compared with the immersive nature of VR. In terms of future adoption, half (51%) of respondents who are interested in buying smart eyewear plan to get Meta AI glasses by Ray-Ban. Another 17% are interested in the rumored Apple glasses, while 10% are interested in Amazon Echo frames.

The Smart Home Era is Here

Want insights on consumer technology trends delivered to your inbox? Join the 451 Alliance.