Source: ManuelVelasco/E+ via Getty images.

Organizational IoT has crossed a threshold. Organizations are no longer debating whether to invest — they are accelerating, consolidating and monetizing. The question has shifted from “should we?” to “how do we scale this effectively?” According to a study conducted by 451 Research from S&P Global Energy Horizons, that transition is well underway, but it is surfacing new complexities around governance, procurement and commercial models.

IoT budgets are being absorbed into broader digital transformation strategies, security has displaced hardware as the top investment priority and outcome-based procurement is gaining serious traction — though traction is unevenly spread across industries and geographies. Notably, nearly two-thirds of IoT-engaged organizations are either already monetizing IoT-generated data or are on a defined path to do so within 24 months. The infrastructure build-out era is giving way to an era of value extraction — and that shift changes everything about how vendors, buyers and operators need to engage.

The Take

The data signals a market in transition, with significant strategic implications for vendors. Security-first positioning is no longer optional — it is table stakes for any IoT vendor operating at scale. AI integration is moving from differentiation to expectation. And the commercial model shift toward outcome-based and as-a-service consumption is real, but adoption is not across the board.

Two notable vertical opportunities stand out: Manufacturing is approaching a monetization inflection point and will need platform and analytics capabilities to execute, while healthcare is in an accelerated catch-up cycle with budget consolidating — a short window for vendors with proven integration and compliance credentials.

The broader mandate: transparency in total cost of ownership (TCO), flexible commercial structures and vertical-specific go-to-market execution are no longer competitive advantages; they are the price of entry.

Summary of findings

Rising spending growth expectations signal a market inflection point. Among organizations using or considering IoT, the mean anticipated spending increase over the next 12 months is 36%, with a median of 26%. Notably, more than half (51%) expect increases of 26% or more. This is not incremental budgeting — it reflects organizations moving from experimentation to scaled deployment, placing IoT firmly in the “strategic spend” category for organizations’ technology leaders.

IoT is losing its stand-alone budget identity — and that may be a good sign. Nearly half of respondents (47%) fund IoT as part of a broader technology or digital transformation budget, while only 39% maintain a dedicated IoT budget. Even more revealing, 33% of respondents say they merged a previously dedicated IoT budget into a broader tech/digital pool in the past year. This convergence with AI and cloud initiatives signals IoT’s integration into organizations’ technology strategy rather than its treatment as a siloed experiment.

IT controls the IoT budget, but operational technology holds influence. The IT department contributes IoT budget in 68% of organizations and is the single primary budget holder in 52% of cases. However, for 43% of organizations, the OT department contributes a significant and growing presence. As IoT deployments increasingly bridge physical operations and digital infrastructure, the IT/OT funding dynamic will define the governance and procurement models that vendors need to address both separately and together.

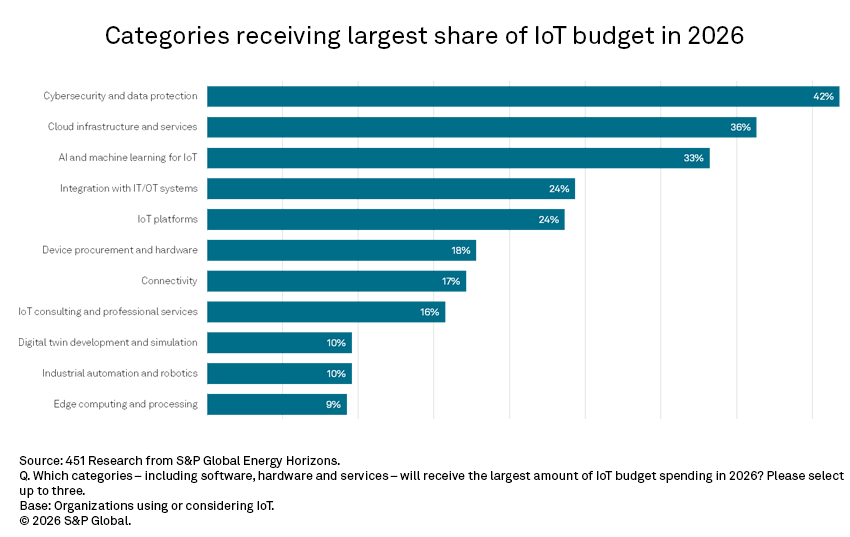

Cybersecurity leads IoT investment priorities in 2026, but AI is rapidly closing the gap — and even pulling ahead in key verticals. Cybersecurity/data protection tops spending categories at 42%, well ahead of cloud infrastructure (36%) and AI/machine learning (33%), while traditional IoT spend areas — hardware (18%) and connectivity (17%) — have fallen to the bottom of the priority stack. As deployments scale, expanding attack surfaces are driving security to the front of the budget queue. But the AI signal is equally important: At just 33% overall, it jumps to 57% for financial services — far above any other vertical — pointing to an accelerating convergence of AI and IoT investment that will increasingly shape both vendor strategy and organizations’ architecture decisions.

Overrun operational costs are nearly as common a growth driver as new use cases. Among those expecting increased IoT spending, 39% cite deploying IoT for new pressing issues, but 38% say ongoing operational costs are running higher than expected. This near-parity suggests that a substantial proportion of IoT spending growth is reactive rather than strategic, a response by organizations absorbing cost surprises from scaling deployments. Vendors should take note that TCO transparency is increasingly a competitive differentiator.

Outcome-based and as-a-service procurement are reaching a tipping point. When asked about outcome-based payment, 89% of respondents either already use it or are at least somewhat likely to adopt it; the percentage is virtually identical for as-a-service consumption (86%). With 38% reporting outcome-based purchasing already in practice (via operating expenditure), the market is clearly moving beyond traditional capital expenditure. The primary resistance is concern about cost uncertainty and budget overrun risk, cited by 46% of reluctant buyers — a solvable problem that vendors with strong service-level agreements and contracting capabilities are positioned to address.

A sharp industry divide reveals where outcome-based procurement is — and is not — taking hold. Global willingness to pay based on business outcomes is 51%, but the crosstab reveals a structural split. Retail (72%) and software & IT services (69%) lead decisively, while government/education (18%) and respondents in Europe, the Middle East and Africa (14%) lag to a degree that goes beyond adoption timing — reflecting fundamental differences in procurement culture, budget process and risk tolerance. Vendors should concentrate outcome-based go-to-market efforts on retail and tech buyers, while treating public sector and the market in Europe, the Middle East and Africa as longer-horizon, different-motion opportunities.

IoT data monetization is transitioning from aspiration to active practice. A third of respondents (34%) currently generate external revenue from IoT data or insights, and another 32% plan to do so within 12-24 months. That means nearly two-thirds of IoT-engaged organizations are either monetizing or are on a defined path to do so. Among monetization strategies, advertising and targeted marketing (37%) and IoT-enabled subscriptions (36%) lead, but the diversity of methods — six approaches cited by at least 29% of respondents — signals a maturing, multimodal monetization landscape.

IoT data monetization exposes a structural divide, with manufacturing emerging as the pivotal near-term opportunity. Software & IT services (57%) and retail (50%) already generate external IoT revenue well above the 34% average. Meanwhile, finance (10%) and government/education (12%) have largely opted out, with 40% and 38%, respectively, reporting no monetization plans — reflecting regulatory and mission-driven constraints rather than an adoption lag.

Manufacturing sits at an inflection point: only 26% monetize today, but 43% plan to within 12–24 months — the highest forward intent of any vertical — with methods skewing toward product and service enhancements over raw data sales, providing a clear signal for platform and analytics vendors targeting industrial buyers.

IoT and the Rise of Smart Spaces

Want insights on IoT trends delivered to your inbox? Join the 451 Alliance.