Source: Westend61/Westend61 via Getty images.

Public cloud spending continues to climb, as does the challenge of tracking and managing costs, with AI experimentation and adoption greatly exacerbating the challenge. As inference and agentic workloads roll into production, structured approaches to FinOps become more important than ever — including developing AI-centric unit cost metrics and expanding the FinOps mandate beyond public cloud infrastructure. A study conducted by 451 Research from S&P Global Energy Horizons examines organizations’ public cloud spending, as well as optimization tools and the impact of generative AI.

The Take

2026 is the year of expanding scope and rising stakes for enterprise FinOps practitioners, with FinOps for AI emerging as the new frontier for cloud cost management as organizations move from experimental to production-scale implementation. The FinOps discipline, which tamed cost complexity in the cloud era, is being called upon again, this time to address financial challenges in the era of AI. However, the standard FinOps tool kit — reserved instance optimization, rightsizing and tagging discipline — does not capture the structural nuances of AI, such as inference endpoints that run continuously and agentic frameworks that generate cascading and hard-to-predict API and GPU consumption.

As a result, 451 Research from S&P Global Energy Horizons expects to see intensified competition in the FinOps market as vendors race to add AI cost metrics to their platforms and organizations seek to demonstrate return on their AI and technology investments. Understanding and communicating the resulting business value is critical for all participants: While cloud provider tools are necessary, they are insufficient for the needs of distributed, hybrid AI deployments and agentic organizations, as illustrated by the rising demand for third-party tools.

Summary of findings

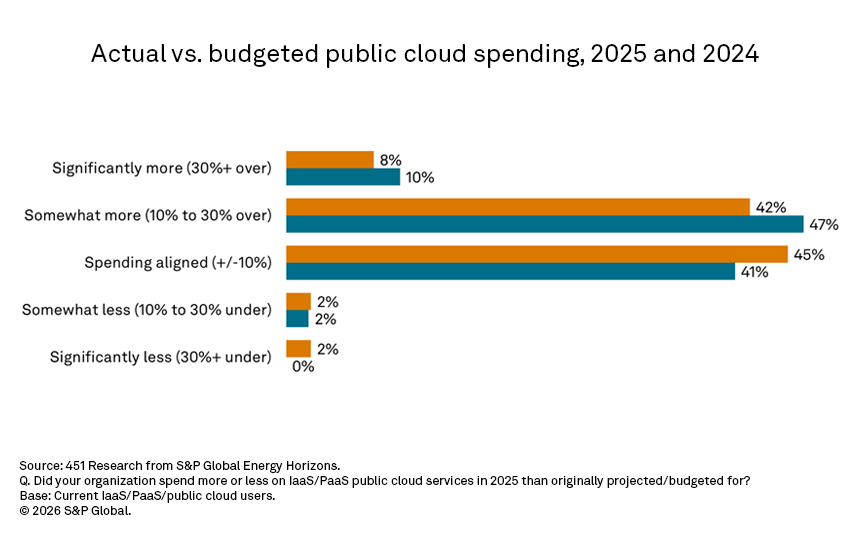

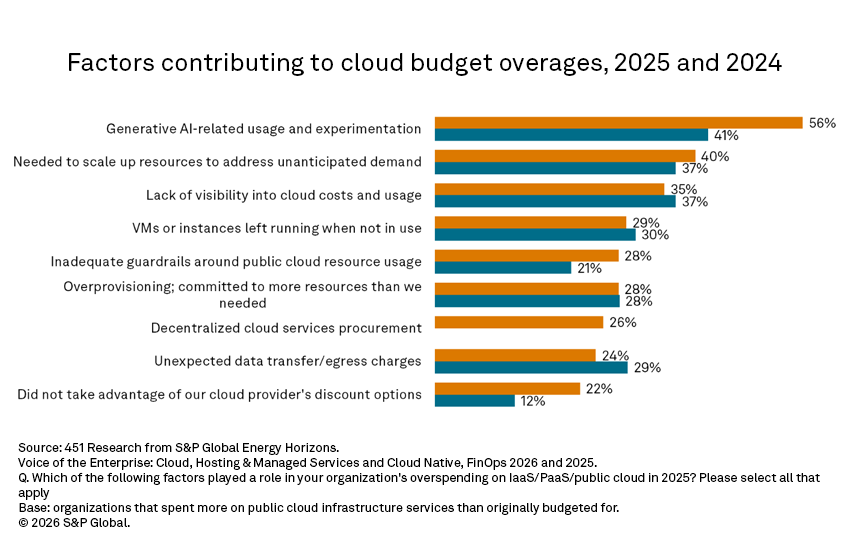

Public cloud budget overage remains an issue, but the situation is improving. Organizations continue to make progress on sticking to their annual public cloud budgets, with “only” half reporting overages at the end of 2025, versus 57% at year-end 2024. As shown in the figures below, generative AI workloads were the top driver of public cloud overspending in 2025, with 56% of organizations highlighting AI experimentation and implementation as a contributing factor, up from 41% in 2024. Notably, in the most recent survey, more than two in five (42%) cite AI use as the primary factor in overspending, by far the top response. At the same time, foundational FinOps challenges persist, with relatively consistent percentages of organizations citing unanticipated resource scaling (40%), lack of visibility (35%) and idle VMs or instances (29%) as contributors to overspending.

Organizations adopt FinOps for AI to address cost and governance challenges. Nearly 60% of organizations are using FinOps for AI for public cloud workloads such as data preparation and management pipelines (62% of the FinOps users surveyed), model fine-tuning and agentic AI workflows (55% each), model training (48%) and inferencing (44%). Organizations with AI workloads in public cloud environments use multiple AI-specific unit metrics, led by the most straightforward: cost per utilized GPU-hour and overall GPU utilization (63%), followed by cost per user/session at the application level and cost per agent action (56% each).

Early-stage public cloud users present rich opportunities for FinOps expansion. More than 60% of mature public cloud users have already implemented FinOps tools, practices and processes, while nearly half of organizations in earlier phases of the cloud journey plan to do so within the next 2 years. This demand trajectory underlies our most recent forecast, which projects a 17% compound annual growth rate (CAGR) for the FinOps market through 2030, up from the 13% CAGR projected in the prior-year forecast, reflecting both the urgency of the AI cost optimization challenge and the expanding addressable market.

FinOps priorities reflect the continuing quest for automated cloud cost management and usage optimization. Planning and forecasting improvement (58%) and usage optimization (56%) remain the top FinOps priorities, but unit economics (48%) is closing the gapand represents the next FinOps maturity threshold. Organizations that move beyond aggregate cloud spending visibility toward per-product, per-customer or per-feature cost attribution will unlock a powerful form of business value measurement — a particularly important component of demonstrating the return on AI investment. Achieving this goal will require investment in tagging discipline, allocation models and integration with accounting systems — areas in which only about a quarter of current FinOps users have reached full maturity.

FinOps branches out beyond public cloud infrastructure. The FinOps Foundation continues to expand its remit by extending FinOps practices to cloud-adjacent IT domains (e.g., software as a service, platform as a service, private cloud, data centers and on-premises IT), and organizations are responding. Nearly 70% of FinOps-enabled organizations’ practices cover SaaS subscriptions (e.g., organizations’ applications and data platforms), while nearly 60% encompass PaaS (e.g., databases and development tools). Other cloud-adjacent domains entering the FinOps fold include AI and machine learning workloads (44%); on-premises IT, private cloud and data centers (39%); sustainability metrics (33%); and containers/Kubernetes (30%).

Organizations are expanding their use of commercial FinOps tools. While hyperscale providers’ own cloud cost management tools remain the default choice, organizations are stepping up adoption of commercial third-party tools, posting just over a 10-percentage-point increase from 45% in 2025 to 56% in 2026. This suggests that native cloud provider tools are necessary but not sufficient, particularly in light of cost governance requirements for distributed, multi-environment and hybrid AI architectures and the FinOps Foundation’s ongoing evolution from a reactive focus on optimization to proactive technology value management.

FinOps continues its transition from a stand-alone process and tooling to an embedded component of organizations’ IT operations. As AI raises the stakes for IT cost optimization, organizations are increasingly integrating FinOps with other business workflows. More than half of organizations (56%) report high FinOps integration with accounting and financial reporting tools in 2026, up from 37% in 2025, followed by cloud and IT service management (54%) and IT asset management (48%).

Cloud Maturity Brings Organizational IT Change

Want insights on cloud computing trends delivered to your inbox? Join the 451 Alliance.