Source: Johnny Greig/Stock Photos | Digital Tablet via iStock by Getty images.

The consumer tablet market has remained stable for so long that it’s downright stagnant at this point. Stuck between the full functionality of PCs and the pocket-sized portability of smartphones, tablets have become a niche product to fulfill a handful of specific use cases while never being a must-have choice for any of them.

Much like a study conducted in Q4 2004 by 451 Research from S&P Global Market Intelligence, consumers continue to prefer devices that will perform all the tasks they require, and tend to lean toward brands they already know. This leads to mostly minor fluctuations in market share, with brand churn netting out in a way that ultimately maintains the status quo.

This blog post presents the findings of a study conducted by 451 Research from S&P Global Energy Horizons, which asked US consumers about current tablet ownership, customer satisfaction and purchasing plans.

Key takeaways from the survey

Apple maintains hold over Generation Z. The positioning within the consumer tablet market is mostly static and unchanging, with Apple (45%), Samsung (25%) and Amazon (18%) standing out as the most-owned tablet brands. No other manufacturer is in the conversation. Apple continued to hold the strongest sway with Generation Z (62%), followed by the Silent Generation (55%), millennials (45%), Generation X (44%) and baby boomers (44%). Samsung’s adoption is more even across the different generations: millennials (31%), Gen X (27%), Gen Z (24%), baby boomers (22%) and the Silent Generation (18%). Amazon, on the other hand, is highest among baby boomers (22%) and the Silent Generation (19%), but then drops off for Gen X (15%), millennials (14%) and Gen Z (12%).

Income also plays a role in adoption. Apple, Samsung and Amazon remain the top brands across all income categories, although there are some differences in rates of ownership within each group. By a 2-1 margin, Apple iPads are owned more by higher-income households (more than $100,000 per year; 63%) than lower-income ones (less than $50,000 per year; 31%). Conversely, Samsung and Amazon tablets show greater ownership among lower-income households (28% and 21%, respectively) than higher-income ones (22% and 12%). The price differential between the brands plays a clear role in their penetration within these different income groups. Similar to the generational breakout, Samsung is the most evenly distributed across these income groups.

Apple’s customer retention reinforces its market dominance. High customer retention rates and low churn help the leading brands stay on top. Apple’s customer retention (86%) is far above both Samsung’s (59%) and Amazon’s (38%). Put another way, the vast majority of Apple owners who plan to buy another tablet in the future say they will buy another iPad, and very few plan to buy from a different tablet manufacturer. While Samsung is second best in this metric, most of its churn goes to Apple. The largest part of Amazon’s churn also goes to Apple, with Samsung as the next-biggest beneficiary. For a product category that is long past its game-changer status, it is no surprise that this market dynamic will likely continue, and no real challengers are likely to emerge to challenge Apple’s dominance.

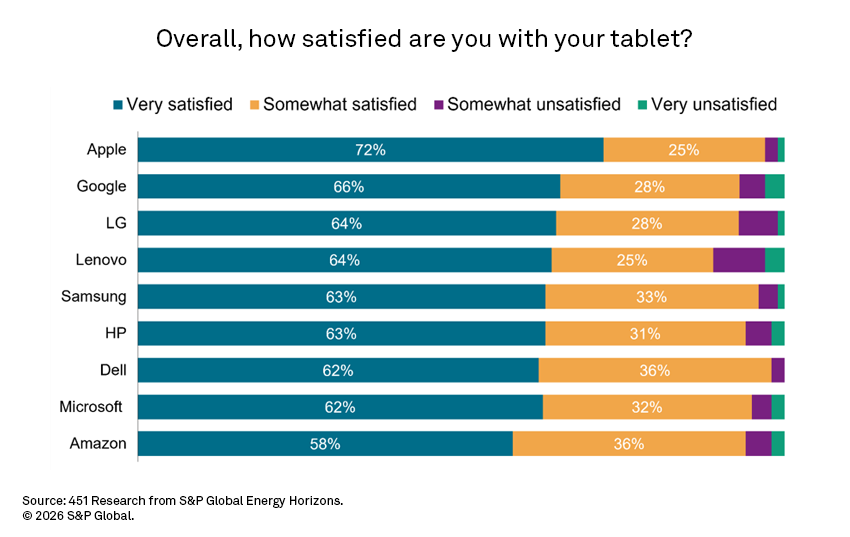

Customer satisfaction is Apple’s not-so-secret weapon. Apple remains the leader in tablet satisfaction, with 72% of current owners saying they are very satisfied with their iPads. Among the other manufacturers, competition is fairly close: Google (66%), Lenovo (64%), Samsung (63%), Microsoft (62%), and Amazon (58%). Interestingly, a few of the defunct tablet brands still have relatively strong satisfaction ratings despite their outdated devices: LG (64%), HP (63%) and Dell (62%). The fact that these older devices still pull solid satisfaction ratings is both a testament to those brands and confirmation that there haven’t been any radical improvements in this product category over the last several years.

Consumers want tablets that will last. We asked respondents what aspects are most important in their purchasing decisions and found that longer battery life (62%), value for the price (57%), reliability (55%) and durability (53%) are what consumers desire most. People expect the electronic devices they buy to work properly. As a result, those basic features are no longer the most important deciding factors. Instead, consumers place higher importance on having durable devices that give them better value for their money and longer lifespans.

The Smart Home Era is Here

Want insights on consumer technology trends delivered to your inbox? Join the 451 Alliance.