Source: mixetto/E+ via Getty images.

Nearly 60% of organizations currently use some type of private cloud infrastructure in their IT environment, typically alongside public cloud resources. Security and operational control considerations are key factors driving private cloud deployments for AI/agentic adoption and data sovereignty use cases.

A survey recently conducted by 451 Research from S&P Global Energy Horizons analyzes organizations’ usage of private cloud infrastructure, including implementation drivers, the types of systems and vendors used, integration with public cloud infrastructure and the impact of AI.

The Take

Previous research notes that latency/performance optimization, data locality and security considerations have raised the profile of private cloud as a deployment venue for AI, sovereign and distributed/edge workloads. Private cloud technology has evolved from basic server virtualization to full-stack systems featuring software-defined infrastructure and unified management and orchestration, substantially mitigating the operational complexity gap vis-à-vis public cloud. As cloud hyperscalers extend their public cloud stacks into organizations’ on-premises environments and hardware/original equipment manufacturers (OEM) vendors enable distributed management and orchestration across IT environments, organizations have options for building flexible, future-proof infrastructure environments to meet various security, performance and governance requirements.

Private cloud defined

In this survey, 451 Research from S&P Global Energy Horizons defined private cloud infrastructure as dedicated IT infrastructure and systems provisioned for the exclusive use of a single organization characterized by the use of virtualization, automation, orchestration and self-service provisioning to deliver resources in a cloud-like manner. Private cloud infrastructure may be managed by the organization or by a third party and can be located in on-premises environments or in third-party colocation facilities.

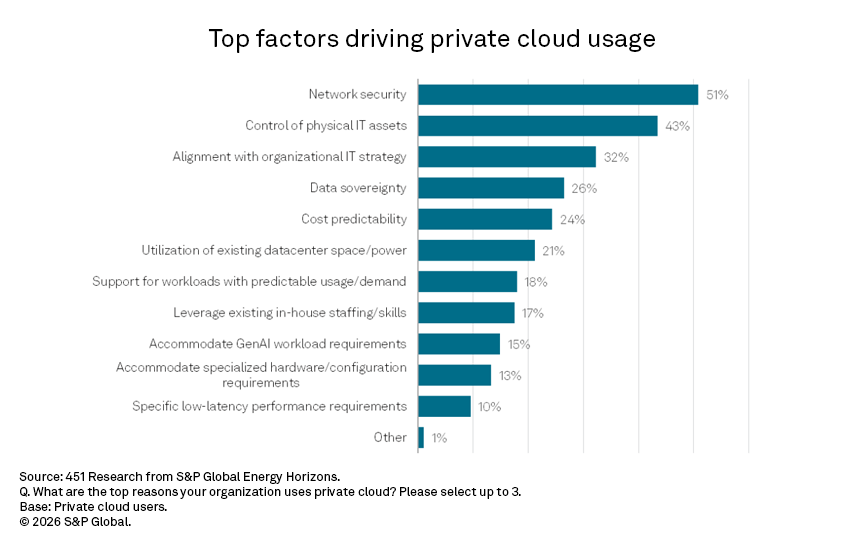

Summary of findings

Security and control considerations drive organizations to private cloud infrastructure. Nearly 60% of organizations have deployed private cloud infrastructure in their IT environments, with those in the finance and healthcare industries posting above-average usage (approximately 75%). Network security emerges as the top decision factor, appearing in just over half of organizations’ top 3 lists. Two closely related factors — physical control of IT assets (43%) and overall alignment with organizational strategy (32%) round out the top three. Data sovereignty, cited in the top three by 26% of organizations as a top-three concern and a hot topic of late, aligns with security and control concerns. Nearly half of organizations currently in the discovery/proof-of-concept stages of deployment pointed to sovereignty as a key decision factor, suggesting that regulatory and jurisdictional concerns are important triggers for private cloud infrastructure adoption.

Multiple infrastructure architectures coexist in private cloud deployments. A plurality (40%) of organizations’ private cloud estates feature a mix of converged infrastructure (bundled packaging of computer, storage and network devices), hyperconverged infrastructure (storage, compute and network resources integrated into a single software-defined system) and disaggregated infrastructure (decoupled server and storage resources and a dedicated high-speed network fabric managed via a unified software-defined management system). This result reflects a market shift toward more flexible, independently configurable/scalable infrastructure better suited to performance-intensive AI workloads and multi-hypervisor IT environments. Eleven percent of organizations report using disaggregated infrastructure exclusively. Nevertheless, converged and hyperconverged infrastructure will remain part of organizations’ IT environments — current usage stands at 27% and 23%, respectively — to serve standard organizational workloads and edge computing requirements.

Private cloud plays a dominant role in users’ IT infrastructure strategies. The bulk of organizations currently using private cloud infrastructure leverage a balanced mix of private and public cloud resources (40%), while 34% have a private cloud-first approach with limited public cloud use. Nearly 30% of private cloud users surveyed characterize their IT infrastructure approach as public cloud-first (15%) or public cloud-dominant (12%) and use private cloud infrastructure for specific workloads or special use cases.

Current users expect to expand their private cloud footprints. Two-thirds of current private cloud infrastructure users anticipate significant (25%) or moderate (41%) increases in their public cloud footprints during the next two years. AI plays a substantial role: nearly 90% of this cohort points to AI adoption/implementation as having a major or moderate impact on the anticipated private cloud footprint expansion. Interestingly, 63% of private cloud infrastructure users with public cloud-first or public cloud-dominant IT approaches highlight AI as a major-impact factor, compared to 45% of organizations with private cloud-dominant strategies and 29% of those with mixed private/public approaches. As noted in previous research, diverse IT environments are the norm for deployments.

Integration between private infrastructure and public clouds is increasingly common. Organizations using both private and public clouds (40% of private cloud infrastructure users) report substantial integration between the two platforms, with 21% describing their implementations as fully integrated (i.e., automation and intelligent workload management across the entire hybrid estate). Forty-one percent of organizations point to “highly integrated” environments featuring workload portability and unified management and orchestration. Only 3% of organizations describe their deployments as not integrated.

Organizations take a mix-and-match approach to private cloud infrastructure. On average, private cloud IT environments feature 2.5 on-premises/colocation hardware/OEM vendors and 2.4management and orchestration vendors. On the hardware front, Cisco, Dell, IBM, Lenovo and HPE emerge as leading vendors used in organizations’ private cloud infrastructure stacks. For management and orchestration software, organizations leverage a range of private cloud virtualization/infrastructure management, container orchestration and hybrid cloud extension platforms, including solutions from IBM, the cloud hyperscalers (AWS, Azure, Google Cloud and Oracle Cloud Infrastructure), VMware and Red Hat, as well as hardware/OEM vendors’ management/orchestration control planes.

VMware remains an important component in private cloud infrastructure stacks, but organizations seek out alternatives. In the wake of Broadcom’s acquisition of VMware and the subsequent pricing and packaging changes, nearly 90% of organizations’ private cloud infrastructure environments include VMware-based workloads. Thirty-seven percent of organizations plan to maintain the bulk of their VMware workloads and have already transitioned, or plan to transition to the bundled subscription model. The remaining 63% of organizations plan various levels of migration away from the VMware platform. One-quarter of current VMware users are transitioning some workloads to alternate private cloud virtualization/management platforms while maintaining reduced VMware footprints. One-third of organizations are actively evaluating VMware alternatives or already transitioning away from VMware, while 6% remain undecided about the future approach.

Cloud Maturity Brings Organizational IT Change

Want insights on cloud computing trends delivered to your inbox? Join the 451 Alliance.