Source: i-Stockr/iStock via Getty Images.

In the current European energy landscape, datacenters stand out as a promising sector for growth amid a sluggish post-energy-crisis power demand recovery. The increasing need for data storage and AI-driven computational capabilities is driving the expansion of datacenters throughout Europe. However, the growth of this sector is hindered by various constraints related to the power market. These constraints include the availability of renewable electricity supply, limitations in grid distribution and transmission infrastructure, and the overall cost of electricity. Therefore, the growth potential of datacenters is closely tied to the dynamics of the power market and its ability to meet the increasing power demands of the sector.

The present state and future prospects of datacenters

From 2019 to 2023, the average power demand of datacenters in Europe has increased by 4.5 GW (46%), with Germany and the UK being the main contributors to this growth. The FLAP markets (Frankfurt, London, Amsterdam, and Paris) have seen a 41% increase in datacenter demand during the same period. The energy intensity of datacenters is high due to the substantial energy requirements for computing and cooling processes. Moreover, datacenters have been growing in size as digitization expands. In the late 2010s, maximum power demand for datacenters was typically 15-30 MW, but now it ranges from 50-100 MW.

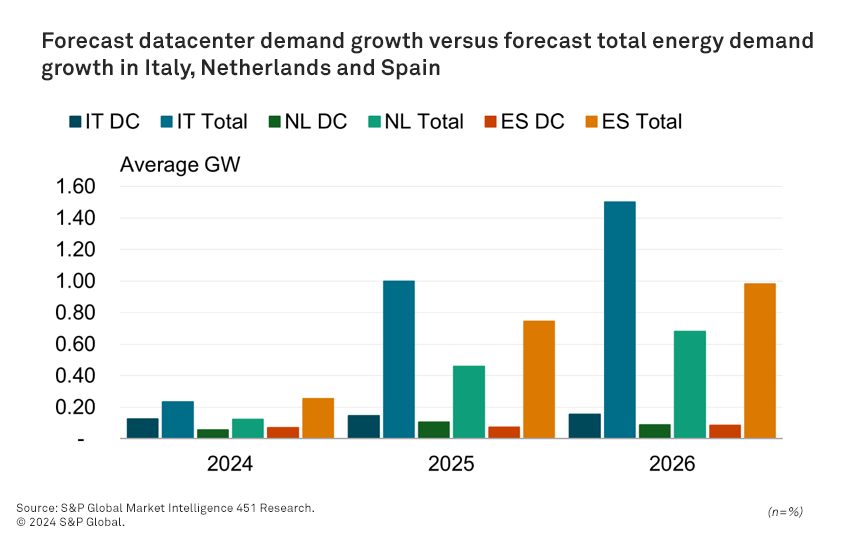

Between 2024 and 2026, datacenter demand is projected to grow by 2.3 GW. This growth significantly contributes to the overall weak year-over-year demand growth for 2024, particularly in Germany. However, Commodity Insights expects a gradual recovery in total electricity demand across these markets in 2025 and 2026, supported by residential demand and the growth of electric vehicles and heat pumps. During this period, datacenter demand is expected to increase year over year, except in the Netherlands, Italy, and Spain, where demand remains relatively unchanged.

The future of datacenter demand depends on two key factors: the adoption rate of generative AI and the efficiency gains driven by innovation. While the full extent of AI applications and their computing power requirements remains uncertain, potential increases in demand from unforeseen AI uses may be balanced by energy efficiency improvements resulting from innovations in equipment and software.

To measure the energy efficiency of datacenters, the power usage effectiveness (PUE) ratio is used. It calculates the total power required to operate the datacenter, including cooling and lighting, divided by the power used for computing. In the past, datacenter facilities had PUEs of 2 or higher, but over time, the PUE has decreased. Different facility types still have varying PUEs. Hyperscale datacenters now achieve PUEs close to 1, with Google reporting a PUE of 1.06 for its datacenter fleet in Q1 2024. The EU’s Energy Efficiency Directive requires datacenters to report their PUE by September 2024 and annually thereafter in May, increasing the focus on energy efficiency in these facilities.

Sustainability

Datacenter providers are not only focusing on energy efficiency but also setting sustainability goals to operate their facilities on renewable energy. For instance, Amazon Web Services aims to achieve global net-zero carbon emissions by 2040 and 100% renewable energy sourcing by 2025. As of 2022, 90% of its operations, including hyperscale datacenters, already run on renewable energy through power purchase agreements and on-site renewables. However, ensuring a constant supply of renewable energy poses challenges due to datacenters’ typical baseload operating profile. Major operators are striving to match their consumption with renewable supply on an hourly basis, although this approach may come with a higher price premium compared to annual matching through guarantees of origin.

Google has developed the “carbon-intelligent computing platform” to shift compute jobs to periods when the grid is cleanest based on day-ahead generation forecasts. This flexibility helps in demand response and load shifting during peak demand periods. As datacenter demand grows, intraday load shifting within local regions and between countries will become crucial. However, challenges arise from varying data sovereignty policies and the coordination required with utilities and grid operators to manage significant demand fluctuations. Installing behind-the-meter battery storage and on-site flexible generation can serve as proxies for real demand shifting.

Up-and-Coming European Markets

Datacenter growth in Europe has mainly focused on the FLAP markets. Although we anticipate year-over-year demand growth in these markets, building new facilities is becoming more challenging in certain areas due to grid limitations, land availability, and power supply adequacy. For instance, the Dutch government is imposing restrictions on hyperscale facility development across the country, which may redirect demand to other European markets.

The growth drivers and constraints for datacenter demand in emerging markets are linked to factors such as renewable electricity supply, grid limitations, regulatory barriers, land availability, electricity costs, and talent availability. The Nordics, particularly Norway and Sweden, are emerging as datacenter regions, with projected energy demand increases of 0.32 GW and 0.26 GW, respectively, from 2024 to 2026. These regions’ growth is driven by a high proportion of renewable energy and comparatively low electricity prices compared to the FLAP region.

Want insights on datacenter trends delivered to your inbox? Join the 451 Alliance.

What is an AI Datacenter?

Want insights on consumer technology trends delivered to your inbox? Join the 451 Alliance.

This content may be AI-assisted and is composed, reviewed, edited and approved by S&P Global in accordance with our Terms of Service.